Crisis Behind the Chaos: Why Consumer Credit May Be the Real Risk to Housing and Economic Stability

While headlines cycle between tariffs on foreign trade, war in Ukraine or Taiwan, new middle east conflicts, and persistent inflation concerns with home prices front and center, the latest markets are pricing in volatility while the Fed holds in a wait and see approach and markets are responding violently to the negative.

But beneath these narratives, there’s a more personal crisis quietly accelerating.

Not one that starts in Beijing or Kyiv. Not one that lives in D.C. or Wall Street.

This one begins at the kitchen table in household budgets already stretched by higher prices, higher rates, and a wave of delayed liabilities coming due. It starts with consumer credit, and its vast ripple effects are being overlooked amidst the noise. But once they start, they tend to spread fast.

It’s not just a policy concern or a line item on an earnings call.

It’s a question of solvency for families, for renters, for first-time home buyers, and eventually for the banks and asset managers who assumed this consumer was stronger than they actually are.

If 2008 was a crisis of over-leveraged homes, 2025 may be the crisis of over-leveraged households.

Household Debt Is Quietly Reaching a Breaking Point

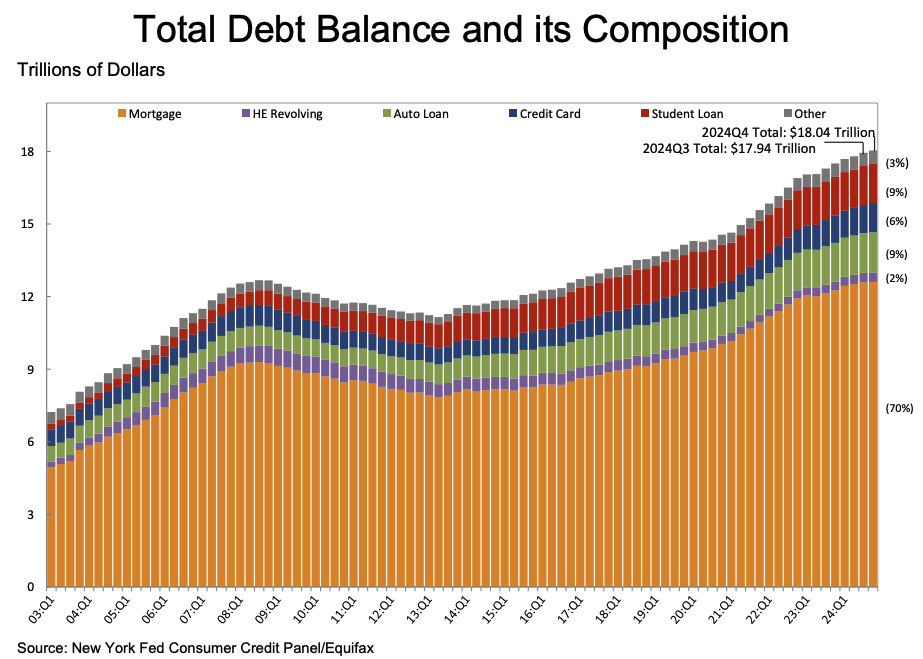

Household debt now exceeds $18 trillion. That’s a 64 percent increase since 2014 and nearly 50 percent higher than it was at the peak of the 2008 financial crisis. This isn’t just about mortgages, although those still make up the bulk of the balance. Credit cards, auto loans, and student debt are all growing. And, unlike mortgage debt, much of this borrowing is happening at variable or elevated rates.

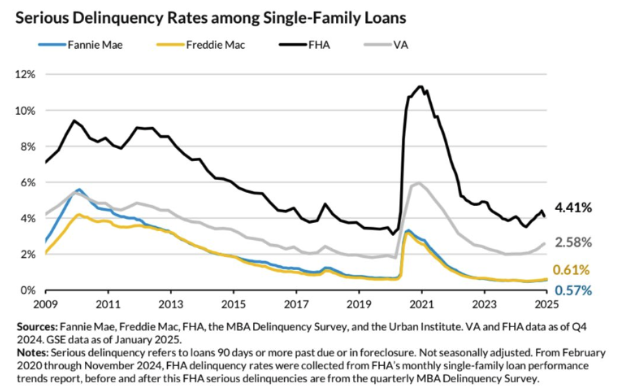

The FHA delinquency story has received headlines recently, with recent figures showing over 15 percent of FHA loans reported as delinquent. But even this isn’t the main event. FHA loans make up roughly 15 percent of total home loans. That means we’re talking about potential early-stage issues on less than 2 percent of the entire mortgage market. Important? Yes. Systemic? Not yet.

So if housing isn’t the flashpoint, what is?

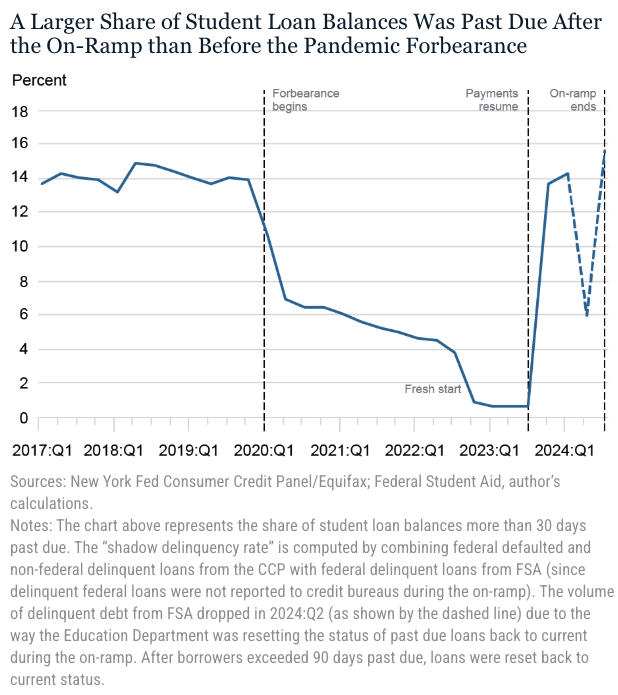

Student Loans Delinquency Surge Hasn’t Fully Hit Yet

After more than three years of paused payments under COVID-era forbearance programs, student loan repayments resumed in late 2023. But to soften the blow, the government enacted a 12-month “on-ramp” through September 2024, during which missed payments would not be reported to credit bureaus.

That ended last fall. And now, in Q1 2025, we’re beginning to see the first wave of student loan delinquencies reported to the credit bureaus again.

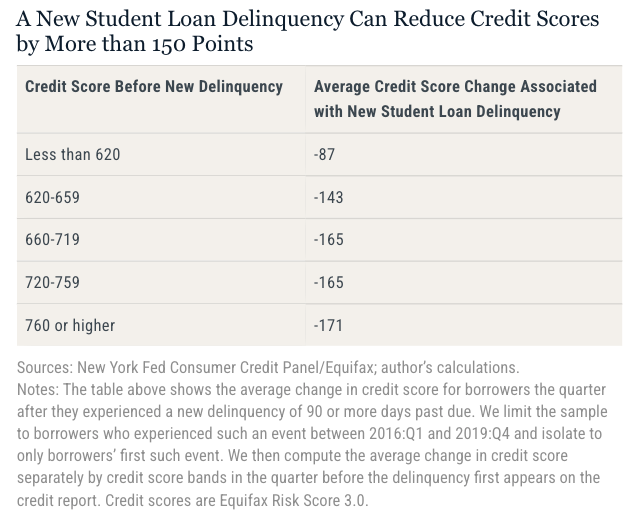

More than nine million borrowers are now at risk of experiencing substantial credit score declines with reports of up to 46% of student borrowers having not resumed payments by September of 2024.

During forbearance, credit scores artificially improved because delinquencies weren’t reported. More than two-thirds of student loan borrowers either maintained or increased their balances between 2019 and 2022, choosing not to pay despite having the option. That period also saw a surge in consumer spending through auto and credit card debt.

Those decisions are now colliding with reality.

When Klarna, Affirm, and BNPL Become Systemic Risk

While student loans were in limbo, a new segment of consumer lending exploded: Buy Now, Pay Later (BNPL). Platforms like Klarna and Affirm fueled a boom in unsecured short-term lending. In many cases, these loans were offered to near-prime or even subprime borrowers and then bundled into securitized investment products.

This isn’t theoretical. Klarna recently announced a partnership with DoorDash. While headlines joked about “Collateralized Burrito Obligations” (CBOs), the underlying risk is no joke.

This is the same playbook as 2005–2007: originate subprime credit, package it, rate it favorably, and sell it as an asset-backed security. Then create synthetic products on top: bets on top of bets.

The difference now? The loans are shorter term, the risk pools are harder to model, and the underlying assets aren’t homes. They’re shoes, takeout, and flights.

Who can be sure where the exposure ends?

Housing Market Stability Is Masking Consumer Fragility

On the surface, the housing market looks healthy:

• Homeowners have record equity.

• Most outstanding mortgages are fixed rate.

• Delinquency rates on mortgage loans remain near historic lows.

But that’s only part of the story.

Those who don’t own a home, or purchased recently at higher rates, are exposed. And if the young renters are still carrying student debt, you’re especially vulnerable.

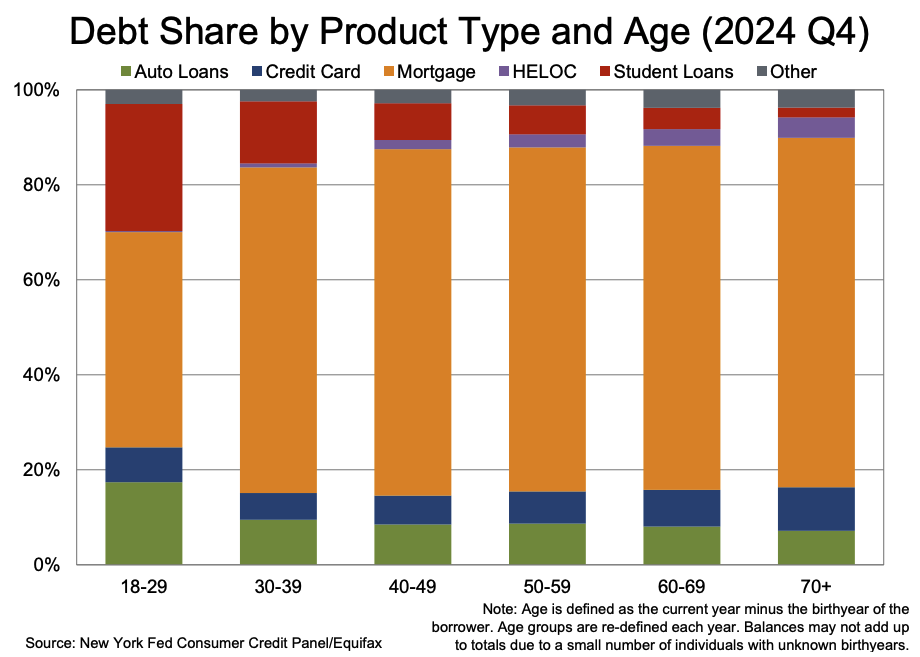

Debt data by age group shows that borrowers under 30 carry disproportionately high balances in credit cards, auto loans, and student debt and very little mortgage exposure or home equity to offset that burden.

Those borrowers don’t have HELOCs to tap. They don’t have fixed housing costs. They don’t have the financial resilience that asset-holding households do.

And if their credit scores drop, their access to everything, from a new lease to a car to a job, can disappear quickly.

This Isn’t 2008. But It Might Be Just As Dangerous

The 2008 crisis was a bottom-up collapse. Risky mortgage lending blew a hole in the foundation, and the financial system came down with it.

This time, the stress is top-down. It’s happening in the consumer sector, slowly cascading from suspended obligations, unsecured credit, inflated scores, and fintech accelerants.

It’s happening through everyday purchases. And it’s hidden, for now, by a housing market that appears stable.

But stability isn’t the same as resilience.

As student loan delinquencies return, BNPL portfolios season, and auto and credit card defaults rise, the cracks will widen. And unlike 2008, we won’t need a housing crash to trigger a recession. We may only need a consumer one.

Final Thoughts

As the housing bubble grew in 2008, new and poorly underwritten mortgage products helped fuel asset appreciation, excessive speculation and far higher credit losses. Mortgage securitization had two major flaws that added risk: nobody along the chain had ultimate responsibility for the results of the underwriting for many securitizations, and the poorly constructed tranches converted a large portion of poorly underwritten loans into Triple A-rated securities. In hindsight, it's apparent that excess speculation and dishonesty on the part of both brokers and consumers further contributed to the problem

The soft landing is still possible. The labor market remains strong. The Fed and administration have tools. Consumers, in aggregate, have built up equity on much less risky home loans - the foundations.

But we must recognize where the real risk is building: in the gap between what people appear able to afford and what they actually can.

If 2008 was about housing bringing down the consumer, could 2025 be the reverse, a consumer credit unwind that eventually pressures housing from the margins?

We should prepare accordingly. Because the next wave starts at your front door, with missed payment, a dropped credit score, and a rising tide of defaults that no one sees until it’s already here.

Sources:

Daniel Mangrum and Crystal Wang, “Credit Score Impacts from Past Due Student Loan Payments,” Federal Reserve Bank of New York Liberty Street Economics, March 26, 2025, https://libertystreeteconomics.newyorkfed.org/2025/03/credit-score-impacts-from-past-due-student-loan-payments/

Daniel Mangrum and Crystal Wang, “Student Loan Balance and Repayment Trends Since the Pandemic Disruption,” Federal Reserve Bank of New York Liberty Street Economics, March 26, 2025, https://libertystreeteconomics.newyorkfed.org/2025/03/student-loan-balance-and-repayment-trends-since-the-pandemic-disruption/.

https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2024Q4

New pieces land here first

One email when something publishes. No drip sequence, no reselling your address.